In this series of posts, I provide a deeper look at common applications of exponential functions that arise in an Algebra II or Precalculus class. In the previous posts in this series, I considered financial applications, radioactive decay, and Newton’s Law of Cooling.

Today, I discuss the logistic growth model, which describes how an infection (like a disease, a rumor, or advertise) spreads in a population. In yesterday’s post, I described an in-class demonstration that engages students while also making the following formula believable:

.

.

I’d like to discuss some observations about this somewhat complicated function that will make producing its graph easier. The first two observations are within reach of Precalculus students.

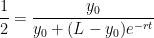

1. Let’s figure out the  intercept:

intercept:

.

.

In other words, the number  represents the initial number of people who have the infection.

represents the initial number of people who have the infection.

2. Let’s figure out the limiting value as  gets large:

gets large:

.

.

As expected, all  people will get the infection eventually. (Of course, Precalculus students won’t be familiar with the $\displaystyle \lim$ notation, but they should understand that

people will get the infection eventually. (Of course, Precalculus students won’t be familiar with the $\displaystyle \lim$ notation, but they should understand that  decays to zero as gets large.

decays to zero as gets large.

3. Let’s now figure out the point of inflection. Ordinarily, points of inflection are found by setting the second derivative equal to zero. Though this can be done for the function  above, it would be a somewhat daunting exercise!

above, it would be a somewhat daunting exercise!

The good news is that the points of inflection can be found quite simply using the governing differential equation, which is

![A' = r A [ L - A] = r L A - r A^2](https://s0.wp.com/latex.php?latex=A%27+%3D+r+A+%5B+L+-+A%5D+%3D+r+L+A+-+r+A%5E2&bg=ffffff&fg=000000&s=0&c=20201002)

Let’s take the derivative of both sides, remembering that  and are constants:

and are constants:

So the second derivative is equal to zero when either  or else

or else  . The first case corresponds to the trivial cases

. The first case corresponds to the trivial cases  and

and  ; these constants are called the equilibrium solutions. The second case is the more interesting one:

; these constants are called the equilibrium solutions. The second case is the more interesting one:

This suggests that, as the infection spreads throughout a population, the curve changes concavity at the time that half of the population becomes infected. In other words, the infection spreads fastest throughout the population at the time when half of the population has been infected.

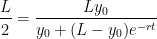

The time at which the point of inflection occurs can be found by setting  and solving for :

and solving for :

.

.

.

.

This technique for finding the points of inflection directly from the differential equation is possible whenever the differential equation is autonomous, which loosely means that the independent variable does not appear on the right-hand side.

![[0,\pi]](https://s0.wp.com/latex.php?latex=%5B0%2C%5Cpi%5D&bg=ffffff&fg=000000&s=0&c=20201002)

, and

![[2\pi/3,\pi]](https://s0.wp.com/latex.php?latex=%5B2%5Cpi%2F3%2C%5Cpi%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![= \displaystyle \bigg[ 3 \theta - 3 \tan \theta \bigg]_{2\pi/3}^{\pi}](https://s0.wp.com/latex.php?latex=%3D+%5Cdisplaystyle+%5Cbigg%5B+3+%5Ctheta+-+3+%5Ctan+%5Ctheta+%5Cbigg%5D_%7B2%5Cpi%2F3%7D%5E%7B%5Cpi%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![= \displaystyle \left[ 3 \pi - 3 \tan \pi \right] - \left[ 3 \left( \frac{2\pi}{3} \right) - 3 \tan \left( \frac{2\pi}{3} \right) \right]](https://s0.wp.com/latex.php?latex=%3D+%5Cdisplaystyle+%5Cleft%5B+3+%5Cpi+-+3+%5Ctan+%5Cpi+%5Cright%5D+-+%5Cleft%5B+3+%5Cleft%28+%5Cfrac%7B2%5Cpi%7D%7B3%7D+%5Cright%29+-+3+%5Ctan+%5Cleft%28+%5Cfrac%7B2%5Cpi%7D%7B3%7D+%5Cright%29+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

. Clearly, we can replace

. Clearly, we can replace  with

with  is trickier. We begin with one of the Pythagorean identities:

is trickier. We begin with one of the Pythagorean identities:

(so that

(so that  ), then

), then  .

. (so that

(so that  ), then

), then  .

.

, so that

, so that  reduces to simply

reduces to simply ![[2\sqrt{3}/3,2]](https://s0.wp.com/latex.php?latex=%5B2%5Csqrt%7B3%7D%2F3%2C2%5D&bg=ffffff&fg=000000&s=0&c=20201002) may be correctly computed as

may be correctly computed as

![[-2,-2\sqrt{3}/3]](https://s0.wp.com/latex.php?latex=%5B-2%2C-2%5Csqrt%7B3%7D%2F3%5D&bg=ffffff&fg=000000&s=0&c=20201002) is incorrectly computed using this formula!

is incorrectly computed using this formula!

![[0,\pi/2) \cup (\pi/2, \pi]](https://s0.wp.com/latex.php?latex=%5B0%2C%5Cpi%2F2%29+%5Ccup+%28%5Cpi%2F2%2C+%5Cpi%5D&bg=ffffff&fg=000000&s=0&c=20201002) to avoid the vertical asymptote at

to avoid the vertical asymptote at  . This portion of the graph of

. This portion of the graph of  . This is perhaps not surprising since, when both are defined,

. This is perhaps not surprising since, when both are defined,  and

and  are reciprocals.

are reciprocals.

matches that of

matches that of  , we have the convenient identity

, we have the convenient identity .

. .

. — that is, for

— that is, for  and

and  .

. can be thought about in three different ways.

can be thought about in three different ways. .

. 2. We have the limits

2. We have the limits .

. . From this derivative,

. From this derivative,  about

about  can be computed:

can be computed:

gives a somewhat more tractable way of approximating

gives a somewhat more tractable way of approximating

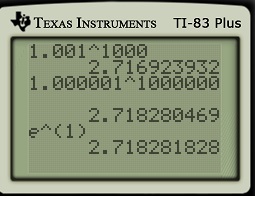

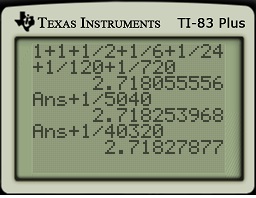

get very small very quickly, leading to rapid convergence. Indeed, with only terms up to

get very small very quickly, leading to rapid convergence. Indeed, with only terms up to  , this approximation beats the above approximation with

, this approximation beats the above approximation with  . Adding just two extra terms comes close to matching the accuracy of the above limit when

. Adding just two extra terms comes close to matching the accuracy of the above limit when  .

.

dollars are invested at interest rate

dollars are invested at interest rate  .

. is equal to

is equal to  , so that

, so that .

.

.

. .

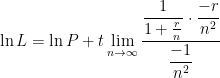

.![\ln L = \displaystyle \ln \left[ \lim_{n \to \infty} P \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+P+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

is continuous, we can

is continuous, we can![\ln L = \displaystyle \lim_{n \to \infty} \ln \left[ P \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cln+%5Cleft%5B+P+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln L = \displaystyle \lim_{n \to \infty} \left[ \ln P + \ln \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%5B+%5Cln+P+%2B+%5Cln+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln L = \displaystyle \lim_{n \to \infty} \left[ \ln P + nt \ln \left( 1 + \frac{r}{n} \right)\right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%5B+%5Cln+P+%2B+nt+%5Cln+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

, as so we may apply L’Hopital’s Rule. Taking the derivative of both the numerator and denominator with respect to

, as so we may apply L’Hopital’s Rule. Taking the derivative of both the numerator and denominator with respect to  , we find

, we find

and

and

.

.

with

with  . Also, replace

. Also, replace  . Then we obtain

. Then we obtain

![rt = \displaystyle \lim_{n \to \infty} \ln \left[ \left(1 + \frac{r}{n} \right)^{n} \right]^t](https://s0.wp.com/latex.php?latex=rt+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cln+%5Cleft%5B+%5Cleft%281+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bn%7D+%5Cright%5D%5Et&bg=ffffff&fg=000000&s=0&c=20201002)

![rt = \displaystyle \ln \left[ \lim_{n \to \infty} \left(1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=rt+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

.![\ln L = \displaystyle \ln \left[ \lim_{h \to 0} \left( 1 + h \right)^{1/h} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bh+%5Cto+0%7D+%5Cleft%28+1+%2B+h+%5Cright%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

. .

. :

:

![e^1 = \exp \left[ \displaystyle \lim_{h \to 0} \ln (1 + h)^{1/h} \right]](https://s0.wp.com/latex.php?latex=e%5E1+%3D+%5Cexp+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bh+%5Cto+0%7D+%5Cln+%281+%2B+h%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

is continuous, we can

is continuous, we can![e = \displaystyle \lim_{h \to 0} \exp \left[ \ln (1 + h)^{1/h} \right]](https://s0.wp.com/latex.php?latex=e+%3D+%5Cdisplaystyle+%5Clim_%7Bh+%5Cto+0%7D+%5Cexp+%5Cleft%5B+%5Cln+%281+%2B+h%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

. for

for  becomes

becomes  . Also, as

. Also, as  , then

, then  .

. . This of course is commonly called the distributive property (and not the commutative property), but the essential idea is that the same answer is obtained whether the multiplications are performed first or if the addition is performed first.

. This of course is commonly called the distributive property (and not the commutative property), but the essential idea is that the same answer is obtained whether the multiplications are performed first or if the addition is performed first. , then

, then  .

. .

. .

. .

. is continuous at an interior point

is continuous at an interior point  , then

, then  .

. are differentiable, then

are differentiable, then  .

. .

. .

. .

. is integrable,

is integrable,  .

. .

. and

and  are random variables, then

are random variables, then  .

. .

. .

. .

. ,

,  , and

, and  are sets, then

are sets, then  .

. .

. if

if  . Important special cases are

. Important special cases are  ,

,  , and

, and  .

. . I call this the

. I call this the  .

. ,

,  , etc.

, etc. .

. .

.

.

. .

. .

.