I recently finished the novel Shantaram, by Gregory David Roberts. As I’m not a professional book reviewer, let me instead quote from the Amazon review:

Crime and punishment, passion and loyalty, betrayal and redemption are only a few of the ingredients in Shantaram, a massive, over-the-top, mostly autobiographical novel. Shantaram is the name given Mr. Lindsay, or Linbaba, the larger-than-life hero. It means “man of God’s peace,” which is what the Indian people know of Lin. What they do not know is that prior to his arrival in Bombay he escaped from an Australian prison where he had begun serving a 19-year sentence. He served two years and leaped over the wall. He was imprisoned for a string of armed robberies performed to support his heroin addiction, which started when his marriage fell apart and he lost custody of his daughter. All of that is enough for several lifetimes, but for Greg Roberts, that’s only the beginning.

He arrives in Bombay with little money, an assumed name, false papers, an untellable past, and no plans for the future. Fortunately, he meets Prabaker right away, a sweet, smiling man who is a street guide. He takes to Lin immediately, eventually introducing him to his home village, where they end up living for six months. When they return to Bombay, they take up residence in a sprawling illegal slum of 25,000 people and Linbaba becomes the resident “doctor.” With a prison knowledge of first aid and whatever medicines he can cadge from doing trades with the local Mafia, he sets up a practice and is regarded as heaven-sent by these poor people who have nothing but illness, rat bites, dysentery, and anemia. He also meets Karla, an enigmatic Swiss-American woman, with whom he falls in love. Theirs is a complicated relationship, and Karla’s connections are murky from the outset.

While it was a cracking good read, what struck me particularly were the surprising mathematical allusions that the author used throughout the novel. In this mini-series, I’d like to explore the ones that I found.

In this first installment, the narrator describes a life-or-death situation as he is being choked:

He was a hard man. He didn’t give up. His hands squeezed tighter. My neck was strong and the muscles were well developed, but I knew he had the strength to kill me. My hand reached, groping for the pistol in my pocket. I had to shoot him. I had to kill him. That was all right. I didn’t care. The air in my lungs was spent, and my brain was exploding in Mandelbrot whirls of colored light, and I was dying, and I wanted to kill him.

Shantaram, Chapter 25

Someone being choked to death might be prosaically described as “seeing stars,” but the author instead to choose the more vivid imagery of “exploding in Mandelbrot whirls of colored light.” The Mandelbrot set is a fractal that solves a famous mathematical problem:

And the Mandelbrot set is quite colorful and complex, which might indeed be a better description than “seeing stars” of what might be going through someone’s mind when being choked to death. Although somewhat dated, here’s my favorite Mandelbrot zoom video:

.

. using the quadratic formula; more on that later.) To apply the method of successive approximation, we will rewrite this so that

using the quadratic formula; more on that later.) To apply the method of successive approximation, we will rewrite this so that  , or

, or .

. .

. .

. .

. . Then

. Then

into a calculator, then entering

into a calculator, then entering  , and then repeatedly hitting the

, and then repeatedly hitting the  button.

button. .

. .

. . Unfortunately, if we start with a guess near this root, like

. Unfortunately, if we start with a guess near this root, like  , the sequence unexpectedly diverges from

, the sequence unexpectedly diverges from  but eventually converges to the positive root

but eventually converges to the positive root  :

:

,

, and

and  . With no modesty, I call this one the Quintanilla sequence when I teach my students — the forgotten little brother of the Fibonacci sequence.

. With no modesty, I call this one the Quintanilla sequence when I teach my students — the forgotten little brother of the Fibonacci sequence. , we obtain the characteristic equation

, we obtain the characteristic equation

,

, and

and  are constants to be determined. To find these constants, we plug in

are constants to be determined. To find these constants, we plug in  :

: .

. :

: .

.

and

and  , so that

, so that ,

,

)

)

:

:

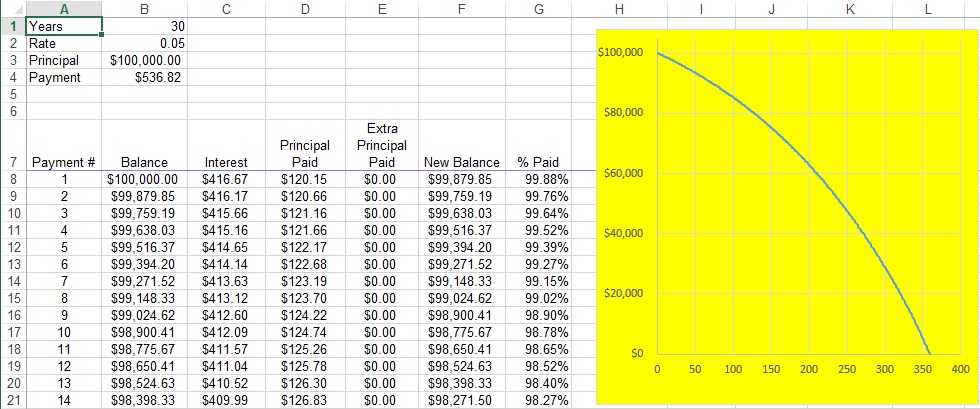

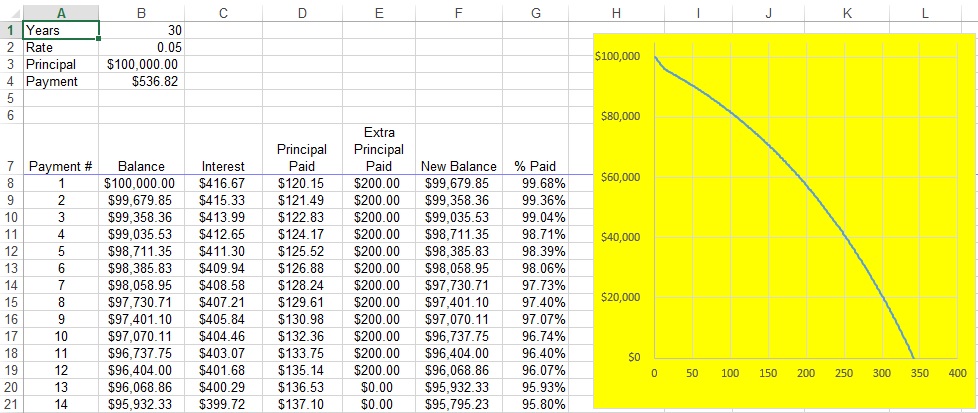

![M = \displaystyle \frac{Pr}{12 \displaystyle \left[1 - \left( 1 + \frac{r}{12} \right)^{-12t} \right]}](https://s0.wp.com/latex.php?latex=M+%3D+%5Cdisplaystyle+%5Cfrac%7BPr%7D%7B12+%5Cdisplaystyle+%5Cleft%5B1+-+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7B12%7D+%5Cright%29%5E%7B-12t%7D+%5Cright%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

. However, in the long run, those payments saved about

. However, in the long run, those payments saved about  !

! (which is greater than 1), and from this product the amount paid is deducted. With this approach — and unlike the approach using calculus — the payment period would be each month and not per year. Therefore, we can write

(which is greater than 1), and from this product the amount paid is deducted. With this approach — and unlike the approach using calculus — the payment period would be each month and not per year. Therefore, we can write

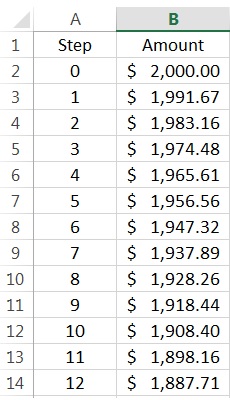

in Cell A2 and

in Cell A2 and  in Cell B2. (In the screenshot below, I changed the format of column B to show dollars and cents.) Next, I entered

in Cell B2. (In the screenshot below, I changed the format of column B to show dollars and cents.) Next, I entered  in Cell A3 and

in Cell A3 and