In my capstone class for future secondary math teachers, I ask my students to come up with ideas for engaging their students with different topics in the secondary mathematics curriculum. In other words, the point of the assignment was not to devise a full-blown lesson plan on this topic. Instead, I asked my students to think about three different ways of getting their students interested in the topic in the first place.

I plan to share some of the best of these ideas on this blog (after asking my students’ permission, of course).

This student submission comes from my former student Andy Nabors. His topic, from Precalculus: compound interest.

What interesting (i.e., uncontrived) word problems using this topic can your students do now?

I would give the students a problem to find out where they should invest their money. They would be given several options with pros and cons and need to choose the best option for them and explain their reasoning. The problem would go something like this:

You are looking to put your graduation money, a total of $2,498, into a savings account. You have gone to several banks and found the interest rates and start-up fees for making an account there. Which bank is offering you the best deal? Which would you choose and why?

| Bank | Interest Rate | Compounded | Start-Up Fee |

| Bank of America | 2.5% | daily | $65 |

| CitiBank | 5% | monthly | $100 |

| Comerica | 3% | weekly | $50 |

| JP Morgan | 1.7% | continuously | $50 |

| Wells Fargo | 3.3% | bi-annually | $0 |

This material is Pre-Cal, so I assume the students are either juniors or seniors, so they may be looking at having to open a bank account of their own in their near future. Then this would be a relevant question for them to look into and figure out what exactly gives them the best option.

How could you as a teacher create an activity or project that involves your topic?

This activity would be similar to one we did in 4050. At the time of this activity, they would not know the formula for compound interest. I would put the students in pairs and pose the question “Suppose you have $1000 that earns 8% interest. How much would you have at the end of 2 years if the interest was compounded: a.)annually b.) biannually c.)quarterly d.)daily”. Then the students would work in pairs to figure out the answers and I would instruct the students to find a pattern as they worked to make it easier. The students would eventually discover the formula for compound interest compounded for any number. They would then be asked how many times the money would have to be compounded to put out the highest total. The students would discover that the higher number, the more total, but as the compounded numbers increased, the difference between the outputs would decrease. So we could then say that there is a limit to how much the output could be, and that limit would be compounded infinitely. Then we could take the limit and find out what the formula is for finding compound interest compounded continuously.

How can technology be used to effectively engage students with this topic?

Students need to know how to do their own research in their future for things like buying a house or car, choosing whether or not to rent or buy, or other things where they are having to find the best deal and fit for them. This activity would have students researching different banks. They would be asked to find out the details on certain banks’ interest rates. They would need to find out about fees and how many times the interest is compounded. They would need information about at least three banks, and then would need to research on independent sites which bank would be the best to start an account with from the banks they chose. Then they would choose a bank for them based on their own findings and calculations, and would choose a bank based on what an online article said. This would let students form their own opinions based on data they found, and weigh that data against the opinions of others. Their findings and opinions may not match up, and that’s why this activity would benefit them. It’s important that students learn to not take the opinions of others as fact, but do their own research to find the best deal.

:

:

![M = \displaystyle \frac{Pr}{12 \displaystyle \left[1 - \left( 1 + \frac{r}{12} \right)^{-12t} \right]}](https://s0.wp.com/latex.php?latex=M+%3D+%5Cdisplaystyle+%5Cfrac%7BPr%7D%7B12+%5Cdisplaystyle+%5Cleft%5B1+-+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7B12%7D+%5Cright%29%5E%7B-12t%7D+%5Cright%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

. However, in the long run, those payments saved about

. However, in the long run, those payments saved about  !

! (which is greater than 1), and from this product the amount paid is deducted. With this approach — and unlike the approach using calculus — the payment period would be each month and not per year. Therefore, we can write

(which is greater than 1), and from this product the amount paid is deducted. With this approach — and unlike the approach using calculus — the payment period would be each month and not per year. Therefore, we can write

in Cell A2 and

in Cell A2 and  in Cell B2. (In the screenshot below, I changed the format of column B to show dollars and cents.) Next, I entered

in Cell B2. (In the screenshot below, I changed the format of column B to show dollars and cents.) Next, I entered  in Cell A3 and

in Cell A3 and

and looking for a pattern.

and looking for a pattern. ,

, and

and  are unknown constants.Why do we guess the solution to have this form? I won’t dive into the details, but this is entirely analogous to constructing

are unknown constants.Why do we guess the solution to have this form? I won’t dive into the details, but this is entirely analogous to constructing  instead of

instead of  , we find that

, we find that .

.

:

:

.

. and solve for

and solve for

![0 = r^n \left( P[1-r] + k \right) - k](https://s0.wp.com/latex.php?latex=0+%3D+r%5En+%5Cleft%28+P%5B1-r%5D+%2B+k+%5Cright%29+-+k&bg=ffffff&fg=000000&s=0&c=20201002)

![k = r^n \left( P[1-r] + k \right)](https://s0.wp.com/latex.php?latex=k+%3D+r%5En+%5Cleft%28+P%5B1-r%5D+%2B+k+%5Cright%29&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \frac{k}{P[1-r] + k} = r^n](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cfrac%7Bk%7D%7BP%5B1-r%5D+%2B+k%7D+%3D+r%5En&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \ln \left( \frac{k}{P[1-r]+k} \right) = n \ln r](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cln+%5Cleft%28+%5Cfrac%7Bk%7D%7BP%5B1-r%5D%2Bk%7D+%5Cright%29+%3D+n+%5Cln+r&bg=ffffff&fg=000000&s=0&c=20201002)

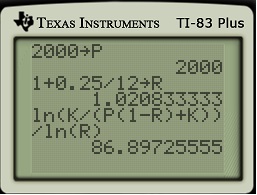

![\displaystyle \frac{ \displaystyle \ln \left( \frac{k}{P[1-r]+k} \right) }{ \ln r} = n](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cfrac%7B+%5Cdisplaystyle+%5Cln+%5Cleft%28+%5Cfrac%7Bk%7D%7BP%5B1-r%5D%2Bk%7D+%5Cright%29+%7D%7B+%5Cln+r%7D+%3D+n&bg=ffffff&fg=000000&s=0&c=20201002)

,

,  , and

, and  :

:

years, which is nearly equal to the value of

years, which is nearly equal to the value of  years

years  , we find

, we find .

. , we find

, we find

, we find

, we find

![A_3 = r \left[ r^2 P - k(1+r) \right] - k](https://s0.wp.com/latex.php?latex=A_3+%3D+r+%5Cleft%5B+r%5E2+P+-+k%281%2Br%29+%5Cright%5D+-+k&bg=ffffff&fg=000000&s=0&c=20201002)

,

,  , and

, and  years is

years is .

.

, has solution

, has solution is the initial amount,

is the initial amount,  is the amount paid per year. In other words, students could be given the formula without the full explanation of where it comes from. After all, many Precalculus textbooks give the formula for Newton’s Law of Cooling (the subject of a future post) with neither derivation nor explanation (though its derivation is nearly identical to the work of yesterday’s post), So I don’t see why also giving students the above formula for paying off credit-card debt isn’t more common.

is the amount paid per year. In other words, students could be given the formula without the full explanation of where it comes from. After all, many Precalculus textbooks give the formula for Newton’s Law of Cooling (the subject of a future post) with neither derivation nor explanation (though its derivation is nearly identical to the work of yesterday’s post), So I don’t see why also giving students the above formula for paying off credit-card debt isn’t more common. years to pay off the debt.

years to pay off the debt. per year for

per year for  years, and so the amount spent is

years, and so the amount spent is .

.

:

:

.

.