The following problem in differential equations has a very practical application for anyone who has either (1) taken out a loan to buy a house or a car or (2) is trying to pay off credit card debt. To my surprise, most math majors haven’t thought through the obvious applications of exponential functions as a means of engaging their future students, even though it is directly pertinent to their lives (both the students’ and the teachers’).

You have a balance of $2,000 on your credit card. Interest is compounded continuously with a rate of growth of 25% per year. If you pay the minimum amount of $50 per month (or $600 per year), how long will it take for the balance to be paid?

In previous posts, I approached this problem using differential equations. There’s another way to approach this problem that avoids using calculus that, hypothetically, is within the grasp of talented Precalculus students. Instead of treating this problem as a differential equation, we instead treat it as a first-order difference equation (also called a recurrence relation):

The idea is that the amount owed is multiplied by a factor

Notice that the meaning of the 25% has changed somewhat… it’s no longer the relative rate of growth, as the 25% has been equally divided for the 12 months.

In yesterday’s post, I demonstrated that the solution of this recurrence relation is

Let’s now study when the credit card debt will actually reach $0. To do this, we see

![0 = r^n \left( P[1-r] + k \right) - k](https://s0.wp.com/latex.php?latex=0+%3D+r%5En+%5Cleft%28+P%5B1-r%5D+%2B+k+%5Cright%29+-+k&bg=ffffff&fg=000000&s=0&c=20201002)

![k = r^n \left( P[1-r] + k \right)](https://s0.wp.com/latex.php?latex=k+%3D+r%5En+%5Cleft%28+P%5B1-r%5D+%2B+k+%5Cright%29&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \frac{k}{P[1-r] + k} = r^n](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cfrac%7Bk%7D%7BP%5B1-r%5D+%2B+k%7D+%3D+r%5En&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \ln \left( \frac{k}{P[1-r]+k} \right) = n \ln r](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cln+%5Cleft%28+%5Cfrac%7Bk%7D%7BP%5B1-r%5D%2Bk%7D+%5Cright%29+%3D+n+%5Cln+r&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \frac{ \displaystyle \ln \left( \frac{k}{P[1-r]+k} \right) }{ \ln r} = n](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cfrac%7B+%5Cdisplaystyle+%5Cln+%5Cleft%28+%5Cfrac%7Bk%7D%7BP%5B1-r%5D%2Bk%7D+%5Cright%29+%7D%7B+%5Cln+r%7D+%3D+n&bg=ffffff&fg=000000&s=0&c=20201002)

That’s certainly a mouthful. However, this calculation should be accessible to a talented student in Precalculus.

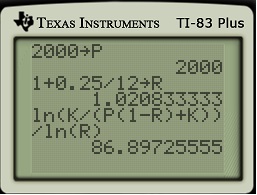

Let’s try it out for

Remembering that each compounding period is one month long, this corresponds to

One thought on “Exponential growth and decay (Part 6): Paying off credit-card debt via recurrence relations”