The following problem in differential equations has a very practical application for anyone who has either (1) taken out a loan to buy a house or a car or (2) is trying to pay off credit card debt. To my surprise, most math majors haven’t thought through the obvious applications of exponential functions as a means of engaging their future students, even though it is directly pertinent to their lives (both the students’ and the teachers’).

You have a balance of $2,000 on your credit card. Interest is compounded continuously with a relative rate of growth of 25% per year. If you pay the minimum amount of $50 per month (or $600 per year), how long will it take for the balance to be paid?

In the previous two posts, I presented the general formula

which can be obtained by solving a certain differential equation. So, if

On the other hand, if the debtor pays $1200 per year, the equation becomes

Today, I’ll give some pedagogical thoughts about how this problem, and other similar problems inspired by financial considerations, could fit into a Precalculus course… and hopefully improve the financial literacy of high school students.

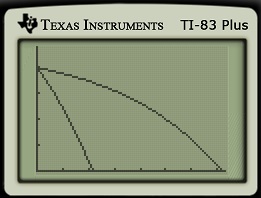

Under the theory that a picture is worth a thousand words, let’s take a look at the graphs of both of these functions:

Under the theory that a picture is worth a thousand words, let’s take a look at the graphs of both of these functions:

Students should have no trouble distinguishing which curve is which. Clearly, by paying $1200 per year instead of $600 per year, the credit card debt is paid off considerably quicker.

Students should have no trouble distinguishing which curve is which. Clearly, by paying $1200 per year instead of $600 per year, the credit card debt is paid off considerably quicker.

There’s another immediate take-away from these graphs — especially the graph for

I believe this to be an important lesson for students to learn before they bury themselves deeply in debt as young adults… and Precalculus provides a natural vehicle for teaching this lesson.

One thought on “Exponential growth and decay (Part 4): Paying off credit-card debt”