Sadly, at least at my university, Taylor series is the topic that is least retained by students years after taking Calculus II. They can remember the rules for integration and differentiation, but their command of Taylor series seems to slip through the cracks. In my opinion, the reason for this lack of retention is completely understandable from a student’s perspective: Taylor series is usually the last topic covered in a semester, and so students learn them quickly for the final and quickly forget about them as soon as the final is over.

Of course, when I need to use Taylor series in an advanced course but my students have completely forgotten this prerequisite knowledge, I have to get them up to speed as soon as possible. Here’s the sequence that I use to accomplish this task. Covering this sequence usually takes me about 30 minutes of class time.

I should emphasize that I present this sequence in an inquiry-based format: I ask leading questions of my students so that the answers of my students are driving the lecture. In other words, I don’t ask my students to simply take dictation. It’s a little hard to describe a question-and-answer format in a blog, but I’ll attempt to do this below.

In the previous posts, I described how I lead students to the definition of the Maclaurin series

which converges to

Step 5. That was easy; let’s try another one. Now let’s try

What’s

Next, to find

Next, we differentiate again:

Hmmm… no obvious pattern yet… so let’s keep going.

For the next term,

For the next term,

Oohh… it’s the factorials again! It looks like

Plugging into the series, we find that

Like the series for

The right-hand side is a special kind of series typically discussed in precalculus. (Students often pause at this point, because most of them have forgotten this too.) It is an infinite geometric series whose first term is $1$ and common ratio $x$. So starting from the right-hand side, one can obtain the left-hand side using the formula

by letting

In other words, in precalculus, we start with the geometric series and end with the function. With Taylor series, we start with the function and end with the series.

Step 6. A whole bunch of other Taylor series can be quickly obtained from the one for

and

we have

____________________

Next, let’s replace

Now let’s take the indefinite integral of both sides:

To solve for the constant of integration, let

Plugging back in, we conclude that

The Taylor series expansion for

Subtracting, we find

My understanding is that this latter series is used by calculators when computing logarithms.

____________________

Next, let’s replace

Now let’s take the indefinite integral of both sides:

To solve for the constant of integration, let

Plugging back in, we conclude that

____________________

In summary, a whole bunch of Taylor series can be extracted quite quickly by differentiating and integrating from a simple infinite geometric series. I’m a firm believer in minimizing the number of formulas that I should memorize. Any time I personally need any of the above series, I’ll quickly use the above steps to derive them from that of

.

. .

. . So

. So  .

. ? Yep, it’s also

? Yep, it’s also  for all

for all  , though we’ll skip the formal proof by induction.

, though we’ll skip the formal proof by induction.

. In other words, the series on the right converges for all values of

. In other words, the series on the right converges for all values of  notation still doesn’t have much meaning.

notation still doesn’t have much meaning.

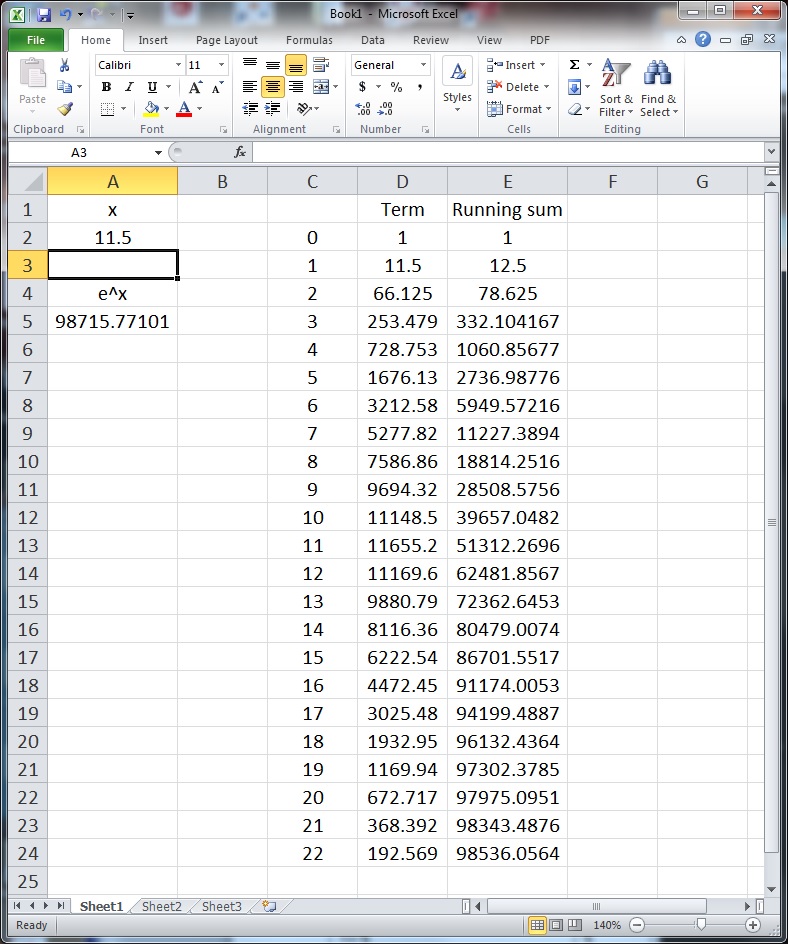

term and that about ten or eleven terms are needed to get a figure that is as accurate as the

term and that about ten or eleven terms are needed to get a figure that is as accurate as the

and then start getting smaller. I’ll ask my students why this happens, and I’ll eventually get an explanation like

and then start getting smaller. I’ll ask my students why this happens, and I’ll eventually get an explanation like

,

,  ,

,  ,

,  , and

, and  . I then ask my class how these could be used to find

. I then ask my class how these could be used to find  . After some thought, they will volunteer that

. After some thought, they will volunteer that .

. , the series for

, the series for  will converge pretty quickly. (Some students may volunteer that the above product is logically equivalent to turning

will converge pretty quickly. (Some students may volunteer that the above product is logically equivalent to turning  into binary.)

into binary.) .

. ,

, can be any number.

can be any number. .

. .

. .

. , which is so “flat” near $x=0$ that every single derivative of

, which is so “flat” near $x=0$ that every single derivative of  at

at  .

. is the

is the  coordinate at

coordinate at  .

. is the slope of the curve at

is the slope of the curve at  is a measure of the concavity of the curve at — you guessed it —

is a measure of the concavity of the curve at — you guessed it —  is an even more subtle description of the curve… once again, at

is an even more subtle description of the curve… once again, at  ,

,  ,

,  ,

,  , and

, and  .

. , and start differentiating. Remember that

, and start differentiating. Remember that  ,

,  ,

,  , and

, and  are constants.

are constants.

. Therefore, it must be that

. Therefore, it must be that  .

. , and so

, and so  . Since

. Since  .

. , and so

, and so  . Since

. Since  , or

, or  .

. , and so

, and so  . Since

. Since  , or

, or  .

. , and so

, and so  . Since

. Since  , or

, or  .

. .

. by

by  . Where did the

. Where did the  , and so

, and so .

. by

by  . The number

. The number  , and so

, and so .

. .

. and

and  .

. and

and  .

. .

. term has a coefficient involving the third derivative of

term has a coefficient involving the third derivative of  and the last term is multiplied by

and the last term is multiplied by  .

. where have we seen those before? Oh yes, the

where have we seen those before? Oh yes, the  ,

,  ,

,  ,

,  , and

, and  is defined to be

is defined to be  .

. notation:

notation: .

. are used over and over again in higher mathematics.

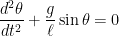

are used over and over again in higher mathematics. A good working knowledge of Taylor series is necessary for computing series solutions of ordinary differential equations.

A good working knowledge of Taylor series is necessary for computing series solutions of ordinary differential equations. are used over and over again. For example, the

are used over and over again. For example, the  ,

, is the acceleration due to gravity and

is the acceleration due to gravity and  is the length of the pendulum. This differential equation cannot be solved exactly, and its solution is

is the length of the pendulum. This differential equation cannot be solved exactly, and its solution is  , so that the differential equation becomes

, so that the differential equation becomes ,

, term, we now have a second-order differential equation with constant coefficients, which can be solved in a straightforward manner using standard techniques from differential equations. If

term, we now have a second-order differential equation with constant coefficients, which can be solved in a straightforward manner using standard techniques from differential equations. If  and

and  (i.e., the pendulum is pulled a small angle

(i.e., the pendulum is pulled a small angle  and is then released), the solution is

and is then released), the solution is .

. , it doesn’t draw a unit circle, trace out an angle of

, it doesn’t draw a unit circle, trace out an angle of  in standard position, and find the

in standard position, and find the  coordinate of the terminal point. Instead, the calculator converts

coordinate of the terminal point. Instead, the calculator converts

, and (as I’ll discuss) the Maclaurin series for

, and (as I’ll discuss) the Maclaurin series for  converges much faster than the Maclaurin series for

converges much faster than the Maclaurin series for  at

at  .

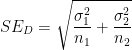

. of two means, where at least one mean does not arise from a small sample, the Student t distribution must be employed. In particular, the number of degrees of freedom for the Student t distribution must be computed. Many textbooks suggest using

of two means, where at least one mean does not arise from a small sample, the Student t distribution must be employed. In particular, the number of degrees of freedom for the Student t distribution must be computed. Many textbooks suggest using

is the standard error associated with the first average

is the standard error associated with the first average  , where

, where  (if known) is the population standard deviation for

(if known) is the population standard deviation for  and

and  is the number of samples that are averaged to find

is the number of samples that are averaged to find  is employed.

is employed. and

and  are similarly defined for the average

are similarly defined for the average  .

. in the numerator is equal to

in the numerator is equal to  . This is the square of the standard error

. This is the square of the standard error  associated with the difference

associated with the difference  .

. ,

, .

.![df = \left( \displaystyle \frac{1}{n_1-1} \left[ \frac{SE_1^2}{SE_1^2 + SE_2^2}\right]^2 + \frac{1}{n_2-1} \left[ \frac{SE_2^2}{SE_1^2 + SE_2^2} \right]^2 \right)^{-1}](https://s0.wp.com/latex.php?latex=df+%3D+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7B1%7D%7Bn_1-1%7D+%5Cleft%5B+%5Cfrac%7BSE_1%5E2%7D%7BSE_1%5E2+%2B+SE_2%5E2%7D%5Cright%5D%5E2+%2B+%5Cfrac%7B1%7D%7Bn_2-1%7D+%5Cleft%5B+%5Cfrac%7BSE_2%5E2%7D%7BSE_1%5E2+%2B+SE_2%5E2%7D+%5Cright%5D%5E2+%5Cright%29%5E%7B-1%7D&bg=ffffff&fg=000000&s=0&c=20201002)

and

and  , so that

, so that![df = \left( \displaystyle \frac{1}{m_1} \left[ \frac{SE_1^2}{SE_1^2 + SE_2^2}\right]^2 + \frac{1}{m_2} \left[ \frac{SE_2^2}{SE_1^2 + SE_2^2} \right]^2 \right)^{-1}](https://s0.wp.com/latex.php?latex=df+%3D+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7B1%7D%7Bm_1%7D+%5Cleft%5B+%5Cfrac%7BSE_1%5E2%7D%7BSE_1%5E2+%2B+SE_2%5E2%7D%5Cright%5D%5E2+%2B+%5Cfrac%7B1%7D%7Bm_2%7D+%5Cleft%5B+%5Cfrac%7BSE_2%5E2%7D%7BSE_1%5E2+%2B+SE_2%5E2%7D+%5Cright%5D%5E2+%5Cright%29%5E%7B-1%7D&bg=ffffff&fg=000000&s=0&c=20201002)

. All of these terms are nonnegative (and, in practice, they’re all positive), so that

. All of these terms are nonnegative (and, in practice, they’re all positive), so that  . Also, the numerator is no larger than the denominator, so that

. Also, the numerator is no larger than the denominator, so that  . Finally, we notice that

. Finally, we notice that .

. ,

, . Since

. Since ![[0,1]](https://s0.wp.com/latex.php?latex=%5B0%2C1%5D&bg=ffffff&fg=000000&s=0&c=20201002) , the absolute extrema can be found by checking the endpoints and the critical point(s).

, the absolute extrema can be found by checking the endpoints and the critical point(s). , then

, then  . On the other hand, if

. On the other hand, if  , then

, then  .

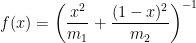

. :

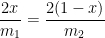

:![f'(x) = -\left( \displaystyle \frac{x^2}{m_1} + \frac{(1-x)^2}{m_2} \right)^{-2} \left[ \displaystyle \frac{2x}{m_1} - \frac{2(1-x)}{m_2} \right] = 0](https://s0.wp.com/latex.php?latex=f%27%28x%29+%3D+-%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7Bx%5E2%7D%7Bm_1%7D+%2B+%5Cfrac%7B%281-x%29%5E2%7D%7Bm_2%7D+%5Cright%29%5E%7B-2%7D+%5Cleft%5B+%5Cdisplaystyle+%5Cfrac%7B2x%7D%7Bm_1%7D+-+%5Cfrac%7B2%281-x%29%7D%7Bm_2%7D+%5Cright%5D+%3D+0&bg=ffffff&fg=000000&s=0&c=20201002)

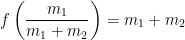

![f \left( \displaystyle \frac{m_1}{m_1+m_2} \right) = \left( \displaystyle \frac{1}{m_1} \frac{m_1^2}{(m_1+m_2)^2} + \frac{1}{m_2} \left[1-\frac{m_1}{m_1+m_2}\right]^2 \right)^{-1}](https://s0.wp.com/latex.php?latex=f+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7Bm_1%7D%7Bm_1%2Bm_2%7D+%5Cright%29+%3D+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7B1%7D%7Bm_1%7D+%5Cfrac%7Bm_1%5E2%7D%7B%28m_1%2Bm_2%29%5E2%7D+%2B+%5Cfrac%7B1%7D%7Bm_2%7D+%5Cleft%5B1-%5Cfrac%7Bm_1%7D%7Bm_1%2Bm_2%7D%5Cright%5D%5E2+%5Cright%29%5E%7B-1%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![f \left( \displaystyle \frac{m_1}{m_1+m_2} \right) = \left( \displaystyle \frac{1}{m_1} \frac{m_1^2}{(m_1+m_2)^2} + \frac{1}{m_2} \left[\frac{m_2}{m_1+m_2}\right]^2 \right)^{-1}](https://s0.wp.com/latex.php?latex=f+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7Bm_1%7D%7Bm_1%2Bm_2%7D+%5Cright%29+%3D+%5Cleft%28+%5Cdisplaystyle+%5Cfrac%7B1%7D%7Bm_1%7D+%5Cfrac%7Bm_1%5E2%7D%7B%28m_1%2Bm_2%29%5E2%7D+%2B+%5Cfrac%7B1%7D%7Bm_2%7D+%5Cleft%5B%5Cfrac%7Bm_2%7D%7Bm_1%2Bm_2%7D%5Cright%5D%5E2+%5Cright%29%5E%7B-1%7D&bg=ffffff&fg=000000&s=0&c=20201002)

and

and  , while the absolute maximum is equal to

, while the absolute maximum is equal to  .

.

is much smaller than

is much smaller than  will be close to

will be close to  .

. ), then

), then  , but no larger.

, but no larger. . I asked my students how I’d write out

. I asked my students how I’d write out  , a numeral with

, a numeral with  consecutive

consecutive  s. So I said, “Who let the dogs out? Me. See:

s. So I said, “Who let the dogs out? Me. See:  , which is clearly a multiple of 9.

, which is clearly a multiple of 9.

and

and  .

. ?

? , then

, then  , which is a multiple of 9.

, which is a multiple of 9. is a multiple of 9, we observe that

is a multiple of 9, we observe that ,

, between the original number and the scrambled number is always a multiple of 9. For example, suppose the volunteer chooses 3417, and suppose the scrambled number is 7431. Then the difference is

between the original number and the scrambled number is always a multiple of 9. For example, suppose the volunteer chooses 3417, and suppose the scrambled number is 7431. Then the difference is

in base-10 notation, and suppose the scrambled number is

in base-10 notation, and suppose the scrambled number is  , where

, where  is a permutation of the numbers

is a permutation of the numbers  . Without loss of generality, suppose that the original number is larger. Then the difference

. Without loss of generality, suppose that the original number is larger. Then the difference

is a multiple of 9.

is a multiple of 9. , then

, then  , and the term in parentheses is guaranteed to be a multiple of 9.

, and the term in parentheses is guaranteed to be a multiple of 9. , then

, then  , and the term in parentheses is guaranteed to be a (negative) multiple of 9.

, and the term in parentheses is guaranteed to be a (negative) multiple of 9. , then

, then  , a multiple of 9.

, a multiple of 9.