In this series of posts, we have seen that the number  can be thought about in three different ways.

can be thought about in three different ways.

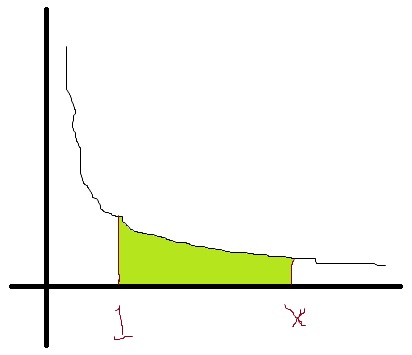

1. defines a region of area 1 under the hyperbola  .

. 2. We have the limits

2. We have the limits

.

.

These limits form the logical basis for the continuous compound interest formula.

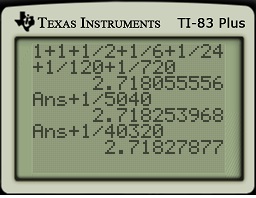

3. We have also shown that  . From this derivative, the Taylor series expansion for

. From this derivative, the Taylor series expansion for  about

about  can be computed:

can be computed:

Therefore, we can let  to find :

to find :

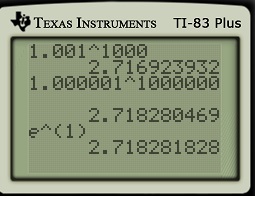

Let’s now consider how the decimal expansion of might be obtained from these three different methods.

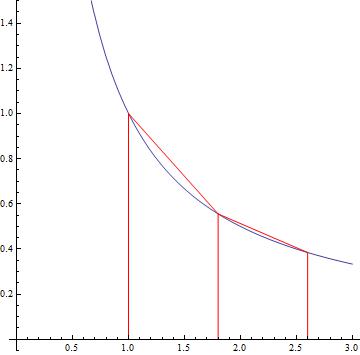

1. Finding using only the original definition is a genuine pain in the neck. The only way to approximate is by trapping the value of using various approximation. For example, consider the picture below, showing the curve and trapezoidal approximations on the intervals ![[1,1.8]](https://s0.wp.com/latex.php?latex=%5B1%2C1.8%5D&bg=ffffff&fg=000000&s=0&c=20201002) and

and ![[1.8,2.6]](https://s0.wp.com/latex.php?latex=%5B1.8%2C2.6%5D&bg=ffffff&fg=000000&s=0&c=20201002) . (Because I need a good picture, I used Mathematica and not Microsoft Paint.)

. (Because I need a good picture, I used Mathematica and not Microsoft Paint.)

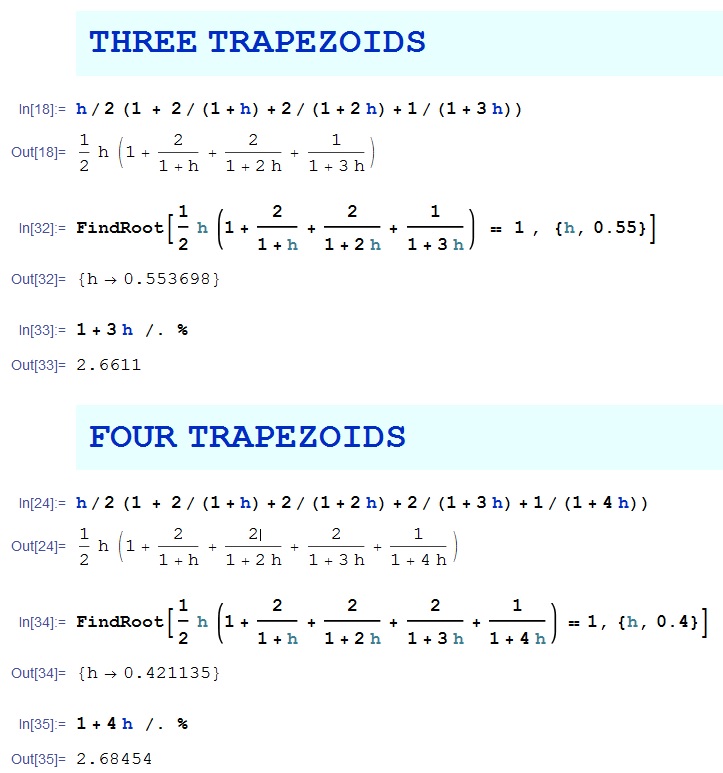

Each trapezoid has a (horizontal) height of  . Furthermore, the bases of the first trapezoids have length

. Furthermore, the bases of the first trapezoids have length  and

and  , while the bases of the second trapezoid of length and

, while the bases of the second trapezoid of length and  . Notice that the trapezoids extend above the hyperbola, so that

. Notice that the trapezoids extend above the hyperbola, so that

However, the number is defined to be the place where the area under the curve is exactly equal to  , and so

, and so

In other words, we know that the area between and  is strictly less than , and therefore a number larger than must be needed to obtain an area equal to .

is strictly less than , and therefore a number larger than must be needed to obtain an area equal to .

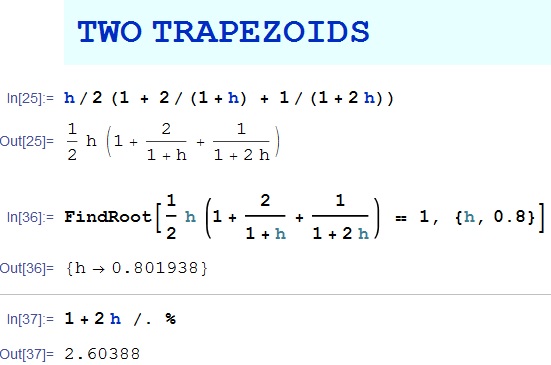

Great, so  . Can we do better? Sadly, with two equal-sized trapezoids, we can’t do much better. If the height of the trapezoids was

. Can we do better? Sadly, with two equal-sized trapezoids, we can’t do much better. If the height of the trapezoids was  and not

and not  , then the sum of the areas of the two trapezoids would be

, then the sum of the areas of the two trapezoids would be

By either guessing and checking — or with the help of Mathematica — it can be determined that this function of is equal to 1 at approximately  , thus establishing that

, thus establishing that  .

.

We can try to better with additional trapezoids. With four trapezoids, we can establish that  .

.

With 100 trapezoids, we can show that  .

.

However, trapezoids can only provide a lower bound on because the original trapezoids all extend over the hyperbola.

However, trapezoids can only provide a lower bound on because the original trapezoids all extend over the hyperbola.

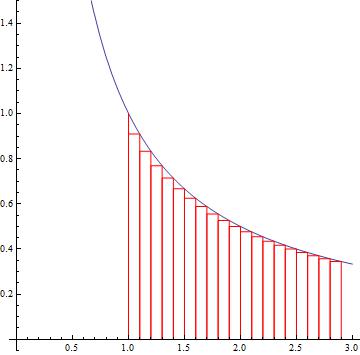

To obtain an upper bound on , we will use a lower Riemann sum to approximate the area under the curve. For example, notice the following picture of 19 rectangles of width  ranging from

ranging from  to

to  .

.

The rectangles all lie below the hyperbola. The width of each one is , and the heights vary from

The rectangles all lie below the hyperbola. The width of each one is , and the heights vary from  to

to  . Therefore,

. Therefore,

In other words, we know that the area between and  is strictly greater than , and therefore a number smaller than must be needed to obtain an area equal to . So, in a nutshell, we’ve shown that

is strictly greater than , and therefore a number smaller than must be needed to obtain an area equal to . So, in a nutshell, we’ve shown that  .

.

Once again, additional rectangles can provide better and better upper bounds on . However, since rectangles do not approximate the hyperbola as well as trapezoids, we expect the convergence to be much slower. For example, with 100 rectangles of width , the sum of the areas of the rectangles would be

It then becomes necessary to plug in numbers for until we find something that’s decently close to yet greater than . Or we can have Mathematica do the work for us:

So with 100 rectangles, we can establish that

So with 100 rectangles, we can establish that  . With 1000 rectangles, we can establish that

. With 1000 rectangles, we can establish that  .

.

Clearly, this is a lot of work for approximating . With all of the work shown in this post, we have shown that  , but we’re not yet sure if the next digit is

, but we’re not yet sure if the next digit is  or

or  .

.

In the next post, we’ll explore the other two ways of thinking about the number as well as their computational tractability.

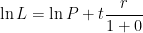

3. The best way to compute

3. The best way to compute

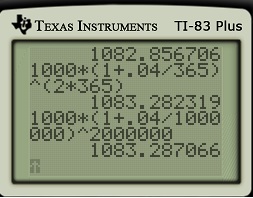

dollars are invested at interest rate

dollars are invested at interest rate  for

for  years with continuous compound interest, then the amount of money after

years with continuous compound interest, then the amount of money after  .

. is equal to

is equal to  .

.

.

. .

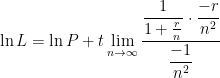

.![\ln L = \displaystyle \ln \left[ \lim_{n \to \infty} P \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+P+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

is continuous, we can

is continuous, we can![\ln L = \displaystyle \lim_{n \to \infty} \ln \left[ P \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cln+%5Cleft%5B+P+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln L = \displaystyle \lim_{n \to \infty} \left[ \ln P + \ln \left( 1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%5B+%5Cln+P+%2B+%5Cln+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln L = \displaystyle \lim_{n \to \infty} \left[ \ln P + nt \ln \left( 1 + \frac{r}{n} \right)\right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%5B+%5Cln+P+%2B+nt+%5Cln+%5Cleft%28+1+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

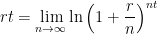

, as so we may apply L’Hopital’s Rule. Taking the derivative of both the numerator and denominator with respect to

, as so we may apply L’Hopital’s Rule. Taking the derivative of both the numerator and denominator with respect to  , we find

, we find

:

:

and

and

.

.

. Also, replace

. Also, replace  with

with  . Then we obtain

. Then we obtain

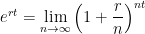

![rt = \displaystyle \lim_{n \to \infty} \ln \left[ \left(1 + \frac{r}{n} \right)^{n} \right]^t](https://s0.wp.com/latex.php?latex=rt+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cln+%5Cleft%5B+%5Cleft%281+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bn%7D+%5Cright%5D%5Et&bg=ffffff&fg=000000&s=0&c=20201002)

![rt = \displaystyle \ln \left[ \lim_{n \to \infty} \left(1 + \frac{r}{n} \right)^{nt} \right]](https://s0.wp.com/latex.php?latex=rt+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Br%7D%7Bn%7D+%5Cright%29%5E%7Bnt%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

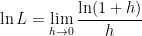

.![\ln L = \displaystyle \ln \left[ \lim_{h \to 0} \left( 1 + h \right)^{1/h} \right]](https://s0.wp.com/latex.php?latex=%5Cln+L+%3D+%5Cdisplaystyle+%5Cln+%5Cleft%5B+%5Clim_%7Bh+%5Cto+0%7D+%5Cleft%28+1+%2B+h+%5Cright%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

. .

. :

:

![e^1 = \exp \left[ \displaystyle \lim_{h \to 0} \ln (1 + h)^{1/h} \right]](https://s0.wp.com/latex.php?latex=e%5E1+%3D+%5Cexp+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bh+%5Cto+0%7D+%5Cln+%281+%2B+h%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

is continuous, we can

is continuous, we can![e = \displaystyle \lim_{h \to 0} \exp \left[ \ln (1 + h)^{1/h} \right]](https://s0.wp.com/latex.php?latex=e+%3D+%5Cdisplaystyle+%5Clim_%7Bh+%5Cto+0%7D+%5Cexp+%5Cleft%5B+%5Cln+%281+%2B+h%29%5E%7B1%2Fh%7D+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

.

. .

. for

for  becomes

becomes  . Also, as

. Also, as  , then

, then  .

. . In today’s post, I’d like to give the more formal derivation using calculus.

. In today’s post, I’d like to give the more formal derivation using calculus. should earn ten times as much interest as

should earn ten times as much interest as  . Since

. Since  is the rate at which the money increases and

is the rate at which the money increases and  is the current amount, that means

is the current amount, that means

in place of

in place of  , with the understanding that

, with the understanding that  ).

). :

:

.

. for computing the value of an investment when interest is compounded

for computing the value of an investment when interest is compounded  as

as  .

. instead of

instead of  . In this way, we can think like an

. In this way, we can think like an  . Then the discrete compound interest formula becomes

. Then the discrete compound interest formula becomes

![A = P\displaystyle \left[ \left( 1 + \frac{1}{m} \right)^m \right]^{rt}](https://s0.wp.com/latex.php?latex=A+%3D+P%5Cdisplaystyle+%5Cleft%5B+%5Cleft%28+1+%2B+%5Cfrac%7B1%7D%7Bm%7D+%5Cright%29%5Em+%5Cright%5D%5E%7Brt%7D&bg=ffffff&fg=000000&s=0&c=20201002)

, except that the name of the variable has changed from

, except that the name of the variable has changed from  . But that’s no big deal: as

. But that’s no big deal: as  and both

and both

,

, , so that we can simply replace

, so that we can simply replace  increases as

increases as  .

. ) that earns 100% interest (so that

) that earns 100% interest (so that  ) for one year (so that

) for one year (so that  ). This isn’t financially realistic, of course, but let’s run with it. Then the compound interest formula becomes

). This isn’t financially realistic, of course, but let’s run with it. Then the compound interest formula becomes

, then

, then  . I’ll usually double-check with my class to make sure that they believe this answer… that $1 compounded once at 100% interest results in $2.

. I’ll usually double-check with my class to make sure that they believe this answer… that $1 compounded once at 100% interest results in $2. , then

, then  .

. , then

, then  .

. , then

, then  .

.

treatment of limit in an honors calculus class or in real analysis. So, mathematically speaking, the above argument should not be considered a proper definition of the number

treatment of limit in an honors calculus class or in real analysis. So, mathematically speaking, the above argument should not be considered a proper definition of the number  .

. .

. .

. ). Then

). Then  .

. .

.

, and so the annual percentage rate would really be 26.824%.

, and so the annual percentage rate would really be 26.824%.