In this series of posts, I consider how two different definitions of the number

- Algebra II/Precalculus: If

dollars are invested at interest rate

for

years with continuous compound interest, then the amount of money after

.

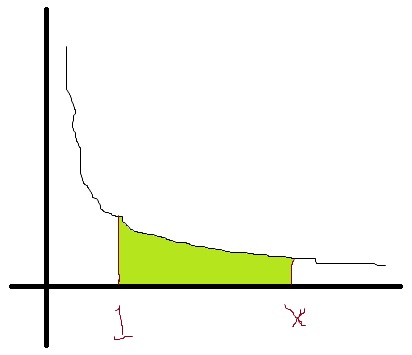

- Calculus: The number

from

to

is equal to

, so that

These two definitions appear to be very, very different. One deals with making money. The other deals with the area under a hyperbola. Amazingly, these two definitions are related to each other. In this series of posts, I’ll discuss the connection between the two.

I should say at the outset that the second definition is usually considered the true definition of

At this point in the exposition, I have justified the formula

At this point in the exposition, I have justified the formula

The bridge between these two formulas is considering increasing values of

1. If interest is compounded annually (

2. If interest i compounded semiannually (

3. If interest is compounded quarterly (

So I ask my class, “What happens to the final amount as interest is compounded more frequently?” They easily observe that the final amount increases somewhat. A natural question, then, is to find how much it can increase. So let’s make the compounding more frequent and let’s see what happens.

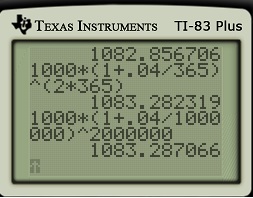

4. Daily: (

5. About twice a minute (

Of course, I perform all of these calculations in real time on a calculator so that students can follow along:

Students quickly observe that the final amount continues to increase as

This provides a natural bridge to continuous compound interest, the topic of tomorrow’s post.

I’ll also note parenthetically that this is why financial institutions are required to disclose the annual percentage rate of a loan (among other things). Otherwise, banks could get away with declaring “Only 2% interest monthly!!” That sounds like 24% annual interest. However,

One thought on “Different definitions of e (Part 3): Discrete compound interest”