Here’s a simple probability problem that should be accessible to high school students who have learned the Multiplication Rule:

Suppose that you play the lottery every day for about 20 years. Each time you play, the chance that you win is

chance in

. What is the probability that, after playing

This is a straightforward application of the Multiplication Rule from probability. The chance of not winning on any one play is

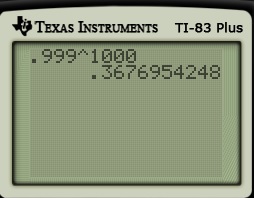

Well, that was easy enough. Now, just for the fun of it, let’s find the reciprocal of this answer.

Hmmm. Two point seven one. Where have I seen that before? Hmmm… Nah, it couldn’t be that.

What if we changed the number

There’s no denying it now… it looks like the reciprocal is approximately

Why is this happening? I offer a thought bubble if you’d like to think about this before proceeding to the answer.

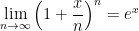

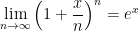

The above calculations are numerical examples that demonstrate the limit

The above calculations are numerical examples that demonstrate the limit

In particular, for the special case when

The first limit can be proved using L’Hopital’s Rule. By continuity of the function

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \lim_{n \to \infty} \ln \left[ \left(1 + \frac{x}{n}\right)^n \right]](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cln+%5Cleft%5B+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \lim_{n \to \infty} n \ln \left(1 + \frac{x}{n}\right)](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+n+%5Cln+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \lim_{n \to \infty} \frac{ \displaystyle \ln \left(1 + \frac{x}{n}\right)}{\displaystyle \frac{1}{n}}](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cfrac%7B+%5Cdisplaystyle+%5Cln+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%7D%7B%5Cdisplaystyle+%5Cfrac%7B1%7D%7Bn%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

The right-hand side has the form

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \lim_{n \to \infty} \frac{ \displaystyle \frac{1}{1 + \frac{x}{n}} \cdot \frac{-x}{n^2} }{\displaystyle \frac{-1}{n^2}}](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cfrac%7B+%5Cdisplaystyle+%5Cfrac%7B1%7D%7B1+%2B+%5Cfrac%7Bx%7D%7Bn%7D%7D+%5Ccdot+%5Cfrac%7B-x%7D%7Bn%5E2%7D+%7D%7B%5Cdisplaystyle+%5Cfrac%7B-1%7D%7Bn%5E2%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \lim_{n \to \infty} \displaystyle \frac{x}{1 + \frac{x}{n}}](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cdisplaystyle+%5Cfrac%7Bx%7D%7B1+%2B+%5Cfrac%7Bx%7D%7Bn%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = \displaystyle \frac{x}{1 + 0}](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+%5Cdisplaystyle+%5Cfrac%7Bx%7D%7B1+%2B+0%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\ln \left[ \displaystyle \lim_{n \to \infty} \left(1 + \frac{x}{n}\right)^n \right] = x](https://s0.wp.com/latex.php?latex=%5Cln+%5Cleft%5B+%5Cdisplaystyle+%5Clim_%7Bn+%5Cto+%5Cinfty%7D+%5Cleft%281+%2B+%5Cfrac%7Bx%7D%7Bn%7D%5Cright%29%5En+%5Cright%5D+%3D+x&bg=ffffff&fg=000000&s=0&c=20201002)

Applying the exponential function to both sides, we conclude that

In an undergraduate probability class, the problem can be viewed as a special case of a Poisson distribution approximating a binomial distribution if there’s a large number of trials and a small probability of success.

In an undergraduate probability class, the problem can be viewed as a special case of a Poisson distribution approximating a binomial distribution if there’s a large number of trials and a small probability of success.

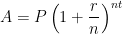

The above calculation also justifies (in Algebra II and Precalculus) how the formula for continuous compound interest

All this to say, Euler knew what he was doing when he decided that